Don't Be Short Intelligence

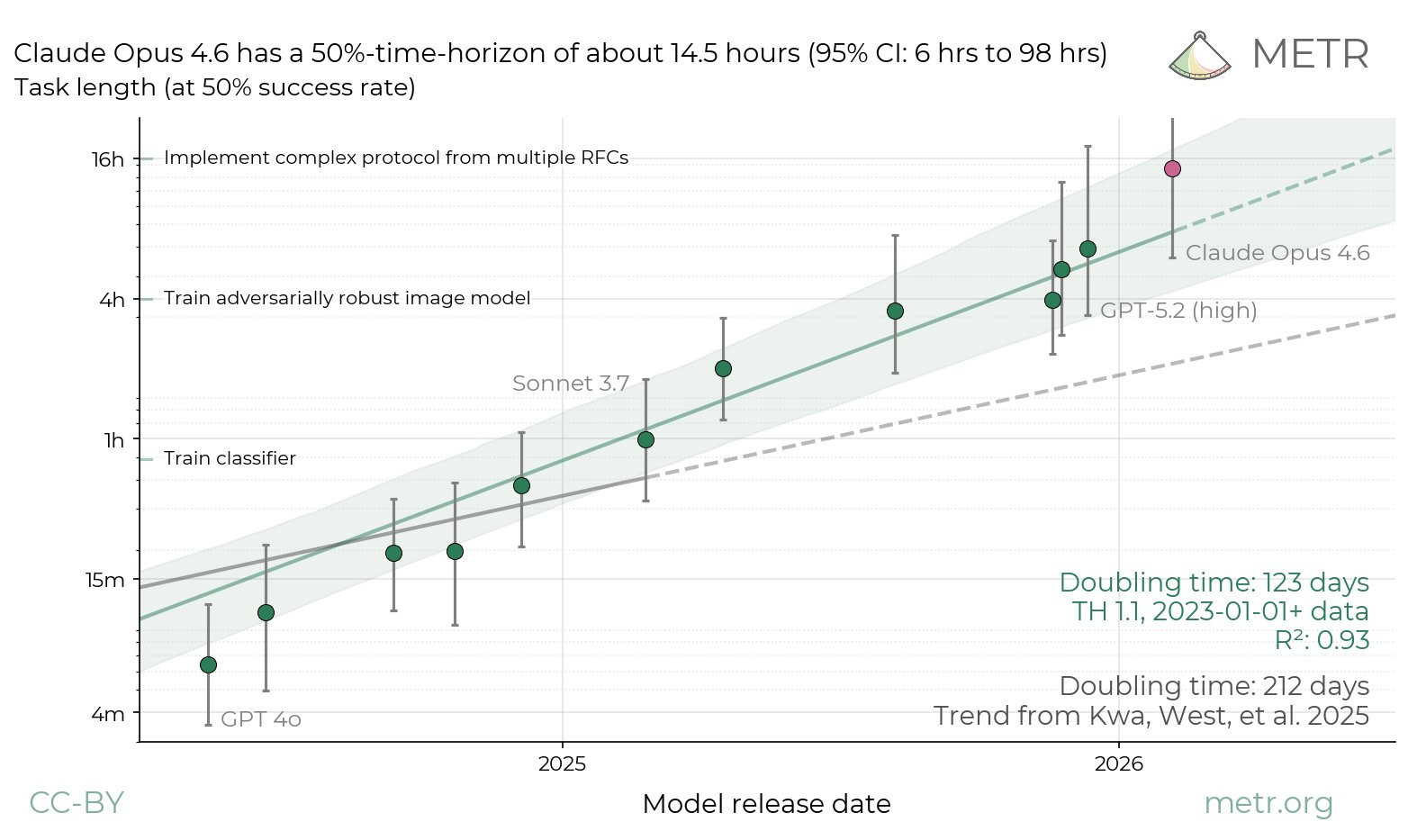

The most important chart in technology right now is AI agents that are performing increasingly long-running tasks. This is trending towards infinity.

We are moving from chatbots to agents that can iterate over complex tasks for hours or days without human intervention.

The common refrain in SaaS is that systems of record like Workday or Salesforce are irreplaceable because of their deep integration into business processes. I am skeptical of this claim on a five-year horizon. In five years, why can’t you ask Claude Code to ‘build me a system of record that replicates every function of my current Salesforce instance, including every custom plugin and workflow’?

Yes, Salesforce is still relevant today as a common standard and schema that agents plug into. But in 5 years, there is a material probability that won’t be true.

There is a real fundamental question about long term durability of any company whose only product output is purely software. It’s not a guarantee these businesses disappear, but there is a substantial non-zero probability they go to 0, and a higher probability that they become structurally impaired.

Addressing The Lump of Labor Fallacy

What about the millennia of evidence that the lump of labor fallacy is wrong?

The lump of labor fallacy does not even attempt to acknowledge what is happening to the nature of work because of AI from first principles. From first principles, AI is not just a new technology that increases economic productivity. It changes the nature of work entirely.

All work - both blue collar and white collar - has two steps:

- Figure out what to do

- Do it

This is true from Sundar Pichai - who determines capital allocation and strategic direction for multi trillion dollar Alphabet - to the janitor, who has to decide whether to sweep left or right first to navigate around the desk in the middle of the room.

Up until the invention of software, substantially all technological innovation improved efficiency of doing the actual work - the wheel, cotton gin, steam engine, car, printing press, etc. Software was a fundamentally new kind of technology, because it allowed humans to program if-then logic to codify human decision making. Software began encroaching on step 1 of work, whereas all prior technology was in the realm of step 2.

It is clear now that transformer based AI systems are approaching a full generalization of step 1. With increasing intelligence and context windows, AI systems will be able to make decisions that Pichai makes, and decisions that the robotic janitor makes.

As you automate an increasing amount of complex decision making itself, there isn’t a higher level of decision making that is unlocked.

This doesn’t mean that all work becomes worthless. At least for the foreseeable future, there is tremendous value in knowing what are the right questions to ask, and how to utilize these systems to their full potential. The system that replaces Oracle as a system of record is less likely to be someone who works at Apple with a mandate to replace Oracle than a net new startup that only ever has a handful of employees who can maximally use these tools to automate decision making at scale and offer a comparable-quality product with 1/100,000th the cost structure.

Software doesn’t sell itself, but when you can cut the cost of software by 100x or more and automate deployment using AI tools, software almost sells itself.

Longs

If we assume the marginal cost of software production is trending toward zero, what businesses are durable? Here are some areas that are less likely to be disrupted by a rapid growth in intelligence. This list is by no means exhaustive.

Financial Services: The moat is brand and user trust. Financial services are by definition just making ledger entires. There isn’t a way to be ‘10x better’ at making ledger entries for mainstream financial services (banking, loans, credit cards, etc.), especially as the cost of producing high quality consumer experiences in software collapses. The clear examples here are Robinhood, Revolut, SoFi, and Nubank.

Crypto: So long as asset prices are volatile, then crypto rails serve a purpose and can produce substantial profits on near-0 cost (e.g. the Solana network captures billions in revenue with minimal costs).

Market Makers: So long as asset prices are volatile, market makers will have a market. This includes both traditional market makers – Jump, Citadel, Virtu, etc. – as well as those focused on non-fungible assets such as Opendoor.

The Physical World: Intelligence doesn’t build silicon or manufacture robots (yet). Durable value exists in the networking supply chain, robotics and defense, and consumer products like Oura and Eightsleep (I’m an angel). The crypto sub-sector of DePIN also falls in this category: Geodnet, Helium, and Hivemapper; I’m long all 3 of these. The best hardware plays are likely to be those where AI can meaningfully improve the product/service, eg Tesla FSD.

Healthcare: given regulatory frictions and physical requirements, AI cannot broadly disrupt healthcare in the same way that it can call centers. There will be opportunities to back AI-native full stack healthcare providers. In general I have a preference to avoid investing in companies that sell into the healthcare system because of the perverse incentives of participants in the existing system (I used to build and sell software into the healthcare system in 2010-2015). Selling into the healthcare system is too slow and expensive and doesn’t allow for compounding capital quickly enough. There are going to be AI-native healthcare companies that rethink care delivery holistically, and these companies can be interesting. Oscar Health is trying to move in this direction, along with 501c3 non-profit integrated health systems like Kaiser and many others. I am an angel in Hone Health, which aims to build the logical end state of DTC healthcare: the ultimate AI doctor.

Marketplaces: As a general statement, intelligence doesn’t change the network effects that emerge around marketplace businesses. This is bullish for companies like DoorDash, who can use AI to reduce costs (deliveries using FSD cars or delivery robots). This is bearish for companies like Uber and Lyft, where intelligence (FSD) changes the supply-side dynamics profoundly.

Brand and SEO (The Information Aggregators): Products where the moat is the human habit and the external link graph. Yahoo Finance and CoinGecko are great examples. There are millions of human-generated links and citations, and tons of UGC (especially YouTube and TikTok videos) that feature these brands and products that intelligence does not displace. As AI accelerates growth in GDP and trading, that provide tailwinds for those businesses in this sector with an API business line.

Shorts

While there is substantial debate today about SaaS, there are easier short opportunities: white collar professional services firms – Infosys, Wipro, WPP, Omnicom, others - are going to plummet as their customers realize they can automate those functions using AI.

SaaS is an interesting question. Consumption based SaaS – eg MongoDB – is likely ok in the near term; seat-based SaaS is in a much more vulnerable position. However, you can imagine a world 5 years from now in which the hyperscalers – in order to take MongoDB’s margin – build an equivalent system with ~1 engineer. From there, it’s not hard to imagine that the hyperscalers undercut the model providers like OpenAI and Anthropic too.

Liquids vs Venture

I think it will be easier to make money – certainly on a risk and liquidity adjusted basis – in public markets than private markets over the next few years for a couple of reasons:

First, AI is going to change the world faster than any technology in human history, both because of its raw power and because it can be made available to everyone because of the mobile + cloud buildout of the last 20 years. Making 10-year dated venture bets under that regime is much riskier today than a decade ago. It is hard to justify paying 30x revenues for a business today if there is an open question on whether the business will have a reason to exist in 5 years.

Second, Amazon and Google and Tesla (and there are arguments to include Microsoft and Apple and Meta) have a straight line path to $10T, and possibly up to $30T, unless the Citrini scenario plays out (white collar workers lose their jobs and stop spending, which impacts Amazon and Google’s primary consumer businesses). Custom chips, insane demand growth for tokens (Tesla + SpaceX + xAI building datacenters in space), and in the case of Amazon, the ability to replace ~1M warehouse workers with robots should propel AMZN and GOOG and TSLA to $10T+ over the next decade. In addition to data centers, Tesla is going after two of the largest physical TAMs in the world with FSD and Optimus.